SALES

With four houses scheduled to close in November and one in December, total sales for 2015 are expected to be on par with 2014. Those sales in the pipeline for the final weeks of the year include two houses in the mid-$2 millions, two priced below $1.5 million, and an attractive recent construction house on a busy corner.

What is different is that there has been only one sale over $4 million since the summer and none expected before year end, unless there is some compelling new inventory forthcoming.

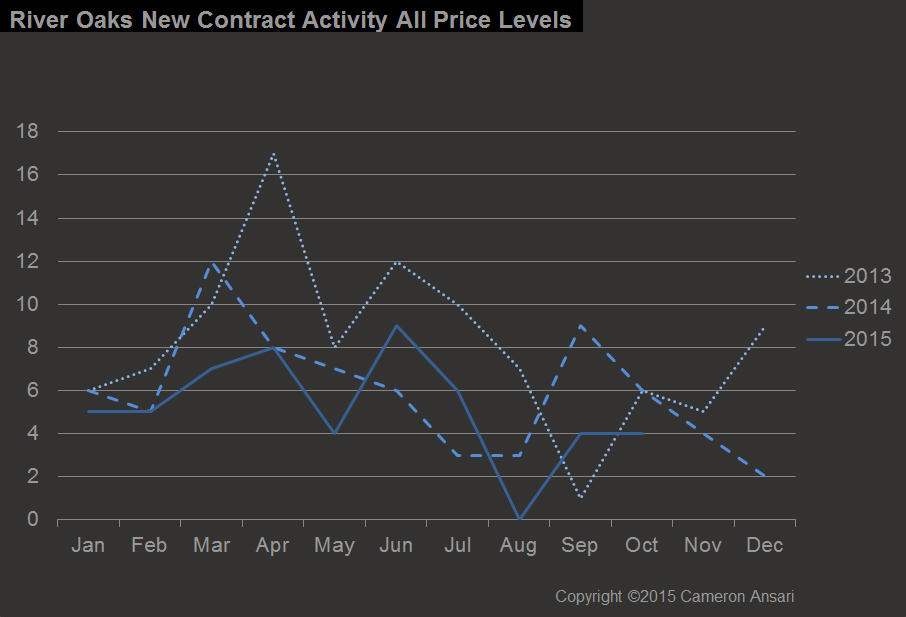

Pending contracts during 2015, the most obvious leading indicator, have been below levels seen in the previous two years (with the exception of a brief peak in the summer).

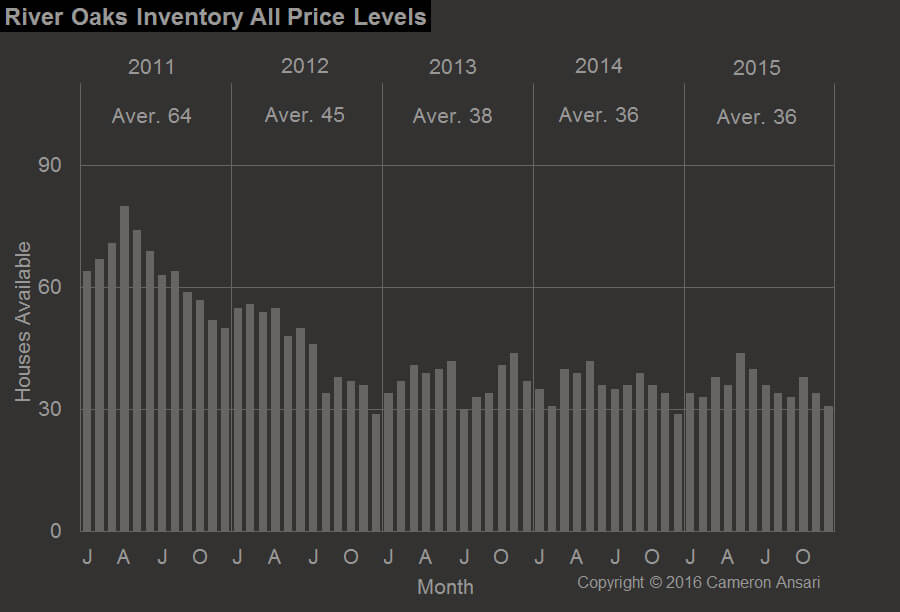

Another leading indicator is the level of showing activity in the various market areas we cover. After a steady climb in viewings of houses by buyers from July through September, there was a marked decline in October in the over $2 million market in all central market areas, with the exception of Memorial. (It was interesting to note that for the price range between $1 million and $2 million showing activity remained steady, if flat.)

By way of explanation, one can conservatively speculate that the state of the energy market — or rather the uncertainty it has created – is largely to blame.

In many past years the final quarter of the year has been the busiest for pending contracts, and for closings too. Bonuses were often announced following the release of third-quarter company results and the conclusion of semi-annual redetermination by their lenders. The tone in the fall of 2015 has been tense.

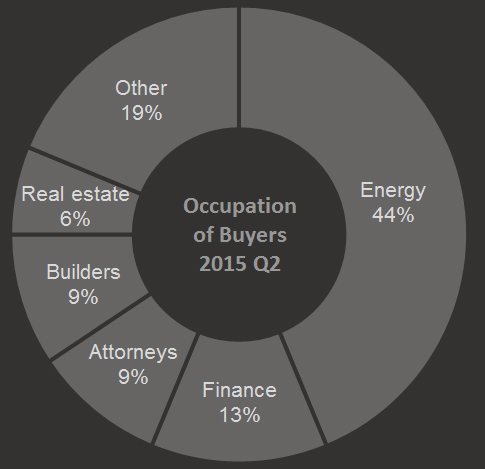

Even through the first half of 2015 energy executives, their lenders and attorneys made up over half the buyers of property in River Oaks. When the statistics for all of 2015 are complete, it is expected that energy executives will continue to be prominent, albeit from other facets of the industry, but also that there will be more diversity of other occupations.